Income from Salary Under the Income Tax Act, 2025

Introduction:

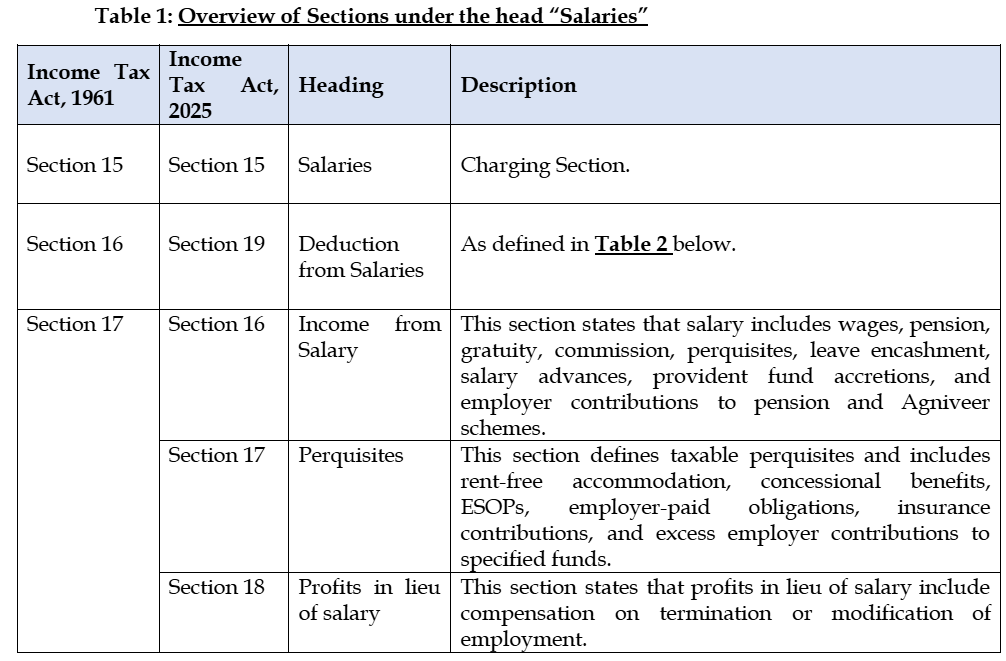

“Salaries” from one or more employers, received or accrued, as the case may be, in a given tax year, are taxed under Section 15 of the Income Tax Act, 2025, which is the charging section.

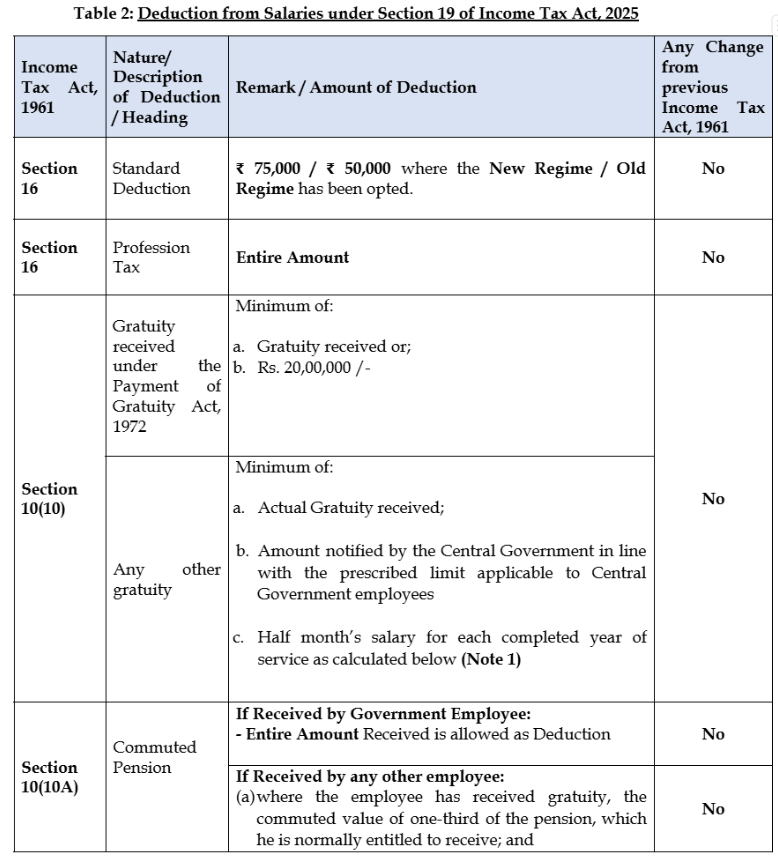

Note 1: ½ × Average Salary × No. of years of service completed

Average Salary (of last 10 months excluding the month of retirement) = Basic Salary (+) Dearness Allowance [in terms] (+) Turnover Commission (%)

Note 2: 15/26 × Average salary of last 3 months × Number of years of service

Note 3: Leave Credit per month (‘p.m.’) = Leave Allowed* (-) Leave taken

*Leave allowed = Maximum 30 days × No. of years of service

Average Salary p.m. = Average Salary (of last 10 months including the month of retirement) = Basic Salary (+) Dearness Allowance [in terms] (+) Turnover Commission (%).

Note 4: Leave encashment salary received during the course of employment is fully taxable in the hands of both Government and non-government employees.

Note 1: The above-mentioned deductions are available in case if the Assessee opts to pay tax under the old tax regime of Income Tax Act, 2025 and these deductions are not allowed if the Assessee opts to pay tax under the New Tax Regime i.e Section 202.

Note 2: Deductions under section 125 (Deduction in respect of contribution to Agnipath Scheme) and Section 124 (Deduction in respect of employer and assessee contribution to pension scheme of Central Government) are still allowed.

Conclusion:

Income from salary is a key component of taxable income under the Income Tax Act, 2025. In conclusion, while the fundamental concept of taxation of salary income remains more or less consistent and same under both the Income Tax Act, 1961 and the Income Tax Act, 2025. A comparative understanding of the two highlights the evolving approach of tax administration towards transparency and ease of compliance of salary taxation. Therefore, a clear understanding of the provisions relating to income from salary under both regimes is essential for taxpayers, employers, and professionals to ensure accurate tax planning and effective compliance with the law.

Authors:

Vishal Kothari

Director | LinkedIn Profile

Nitesh Jha

Manager | LinkedIn Profile

Urvi Gandhi

Associate Consultant |LinkedIn Profile

.svg)