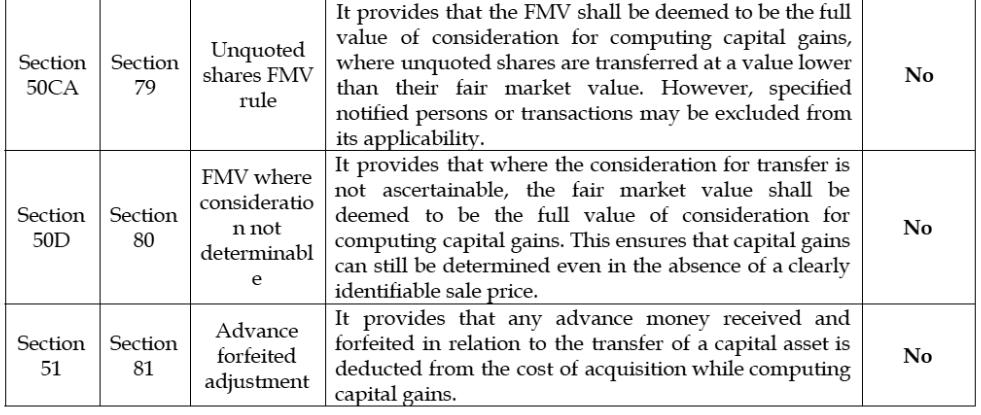

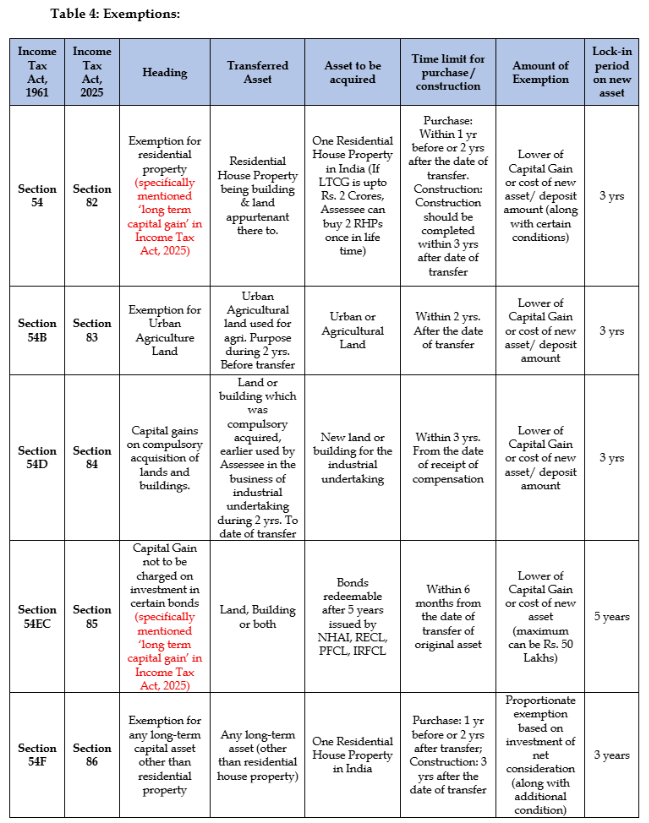

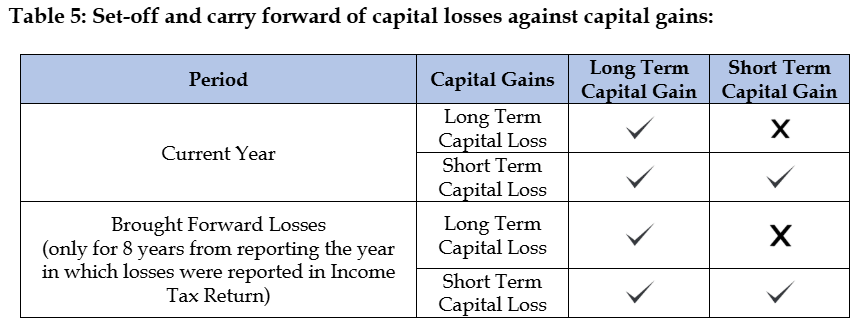

Income from Capital Gains under the Income Tax Act, 2025

Introduction:

‘Capital Gains’ refers to the profit earned on the transfer of a capital asset—such as property, shares, or gold—when it is sold for a price higher than its cost of acquisition. It represents the appreciation in the value of an investment over time and is chargeable to tax.

While income tax generally applies to income of a revenue nature, capital gains constitute a specific carve-in to the Act to bring capital transactions within the tax net. Further, most heads of income are inclusive in nature, specifying certain incomes that are exempt, whereas the head ‘Capital Gains’ is exclusive in nature—only those gains that are specifically covered under its provisions are taxable, and all other capital receipts are deemed to be outside its scope unless expressly brought to tax.

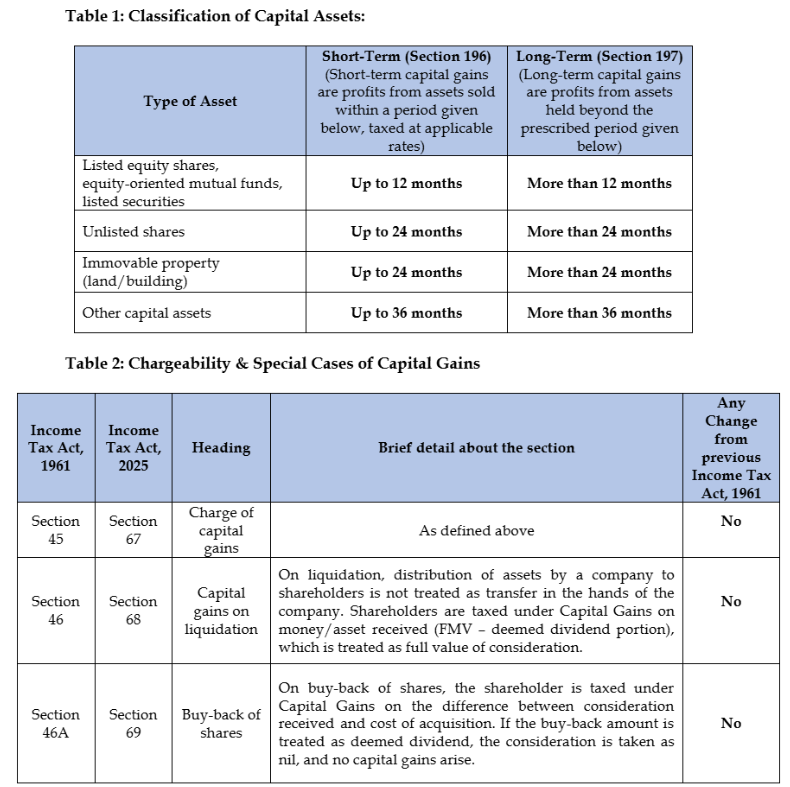

The charging Section 67 of the Income Tax Act, 2025 sets forth the following conditions for a transaction to qualify to be taxed under the provisions of capital gain:

- There must exist a capital asset, being property of any kind such as land, building, shares, securities, or other investments, held by the assessee.

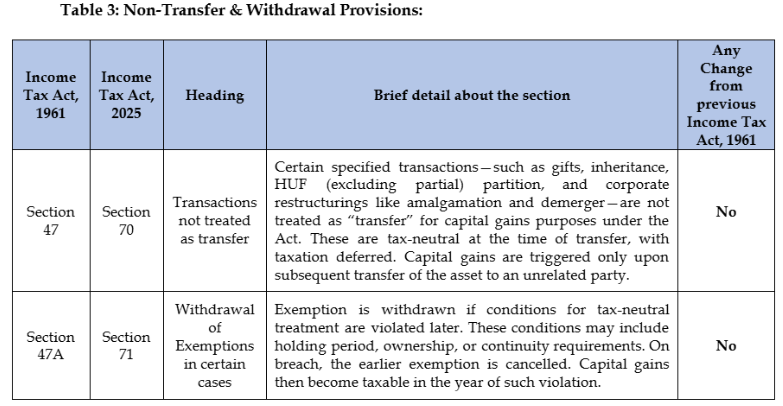

- Such capital asset must be transferred during the relevant tax year, whether by way of sale, exchange, relinquishment, or any other mode recognized under the Act.

- The profits or gains arising from such transfer must not be specifically exempt under any other provisions of the Act, and only such non-exempt gains shall be chargeable to tax.

Capital Asset as defined under Section 2(22) of the Income Tax Act, 2025, includes property of any kind (including FII securities) but excludes stock-in-trade, certain personal movable assets, rural agricultural land, and specified gold-related instruments.

Conclusion:

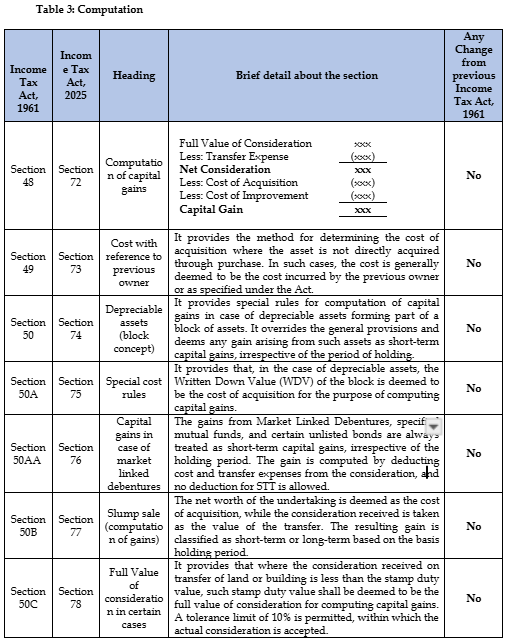

Income under the head ‘Capital Gains’ is an important component of taxable income under the Income Tax Act 2025 India. The Act provides comprehensive provisions covering chargeability, computation, special cases, and exemptions relating to capital assets. A clear understanding of concepts like cost of acquisition, full value of consideration, and applicable reliefs helps taxpayers ensure accurate tax compliance and effective tax planning.

Authors:

Vishal Kothari

Director | LinkedIn Profile

Nitesh Jha

Manager | LinkedIn Profile

Rutwick Ruparelia

Manager

Deveshh Gupta

Consultant |LinkedIn Profile

.svg)